Content

Make a marketing plan

Marketing takes time, money, and preparation. One of the best ways to stay on schedule and on budget is to make a marketing plan. It describes the actions you’ll take to persuade potential customers to buy your products or services.

Your business plan should contain the central elements of your marketing strategy. Your marketing plan turns your strategy into action.

Use these sections in your marketing plan

Most marketing plans cover these topics. As always, use what works best for your business.

Target market

Describe your audience in detail. Look at the market’s size, demographics, unique traits, and trends that relate to demand for your business.

Competitive advantage

Describe what gives your product or service an advantage over the competition. It might be a better product, a lower price, or an excellent customer experience. Sometimes, an environmentally friendly certification or “made in the USA” on your label can be an important factor for customers.

Sales plan

Describe how you’ll literally sell your service or product to your customers. List the sales methods you’ll use, like retail, wholesale, or your own online store. Explain each step your customer takes once they decide to buy.

Marketing and sales goals

Describe your marketing and sales goals for the next year. Common marketing and sales goals are to increase email subscribers, grow market share, or increase sales by a certain percent.

Marketing action plan

Describe how you’ll achieve your marketing and sales goals. List marketing channels you’ll use, like online advertising, radio ads, or billboards. Explain your pricing strategy and how you’ll use promotions. Talk about the customer support that happens after the sale. The federal government regulates advertising and labeling for a number of consumer products, so make sure your advertising is legally compliant.

Budget

Include a complete breakdown of the costs of your marketing plan. Try to be as accurate as possible. You’ll want to keep tracking your costs once you put your plan into action.

-

Target market

-

Competitive advantage

-

Sales plan

-

Marketing and sales goals

-

Marketing action plan

-

Budget

Measure and update your plan

Plan to compare your marketing and sales costs to the revenue it generates. You want to make sure you’re getting a positive return on investment, or ROI.

Some tactics are hard to measure — like print advertising or word-of-mouth campaigns. Get creative and use others’ advice, but be consistent in how you measure the effectiveness of your marketing efforts.

Marketing plans should be maintained on an annual basis, at minimum. Measuring ROI will help you know which part of the plan is working and which part needs to be updated.

Don’t forget about operations

Not everyone agrees on the exact distinctions between marketing and sales, but most people recognize they’re connected. The influence operations has on marketing and sales is often overlooked.

Simple operations elements like your staff uniform, where your product is made, or the product return process contribute to your customer’s experience. That experience shapes how your customers view your company, and can influence whether they’ll become a loyal customer for life or tell their friends to stay away.

Choose how you’ll accept payments

The kinds of payments you accept can impact your marketing and sales, as well as your bottom line. Accept forms of payments that are cost effective, secure, and provide a positive experience for your customers.

You’ll need a business bank account no matter what kinds of payment you choose.

Credit cards

To accept credit and debit cards, you’ll need either a merchant services account with a bank or an account with an independent payment processing company.

You’ll pay small processing fees for each credit or debit card transaction, plus costs for setting up any necessary equipment.

Accepting credit and debit cards exposes you to the risk of fraud, but most vendors provide a certain level of protection for your business. Make sure that you use an EMV (Europay, MasterCard, and Visa) chip reader, which will limit both fraud and your liability.

Checks

You only need a business bank account to accept checks.

You’ll want to create a policy for accepting checks to help you avoid bad or fraudulent checks. Standard practices include only taking checks from well-known or in-state banks, or requiring checks be only for the exact amount owed. You could also use a third party service to help verify the quality of the check.

If a check bounces, your options to get the final payment will vary depending on your location. Some states require businesses to mail a registered letter and allow a designated waiting period to lapse before further action is taken. To get payment for a bounced check, you could end up in small claims court or using a collection agency.

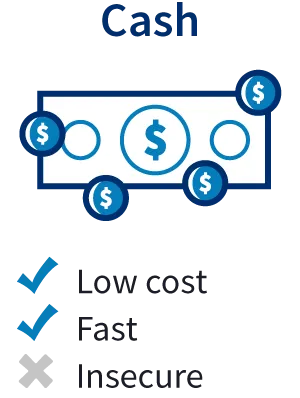

Cash

Many small businesses operate as "cash only" merchants because it’s fast, easy, and inexpensive.

If you accept cash, remember that large sums of cash can add to accounting time and come with an additional security risk. You’ll want a secure way to hold your cash, like a register and a safe.

There are special reporting requirements for cash. The IRS requires you to report if your business gets more than $10,000 in cash, or a cash equivalent, from one buyer as a result of a single transaction or two or more related transactions.

Online payments

If you sell your product or service online, you could accept payment through your website with an online payment service.

Online payment services typically accept credit and debit cards in addition to other popular online money transfer services. You’ll pay fees to in order to accept payments online, just like accepting credit cards in a physical location.

Online payment services require a virtual shopping cart to calculate the total, tax, and shipping costs of an order, in addition to collecting customer account and shipping information. Some online payment service providers offer free shopping cart services to businesses.

Example marketing plan